Many service-based businesses have ambitious growth goals, but lack clear visibility into the financial signals that determine whether they’re on track. Tracking the right cash flow KPIs helps business owners understand whether they have enough liquidity to operate, invest and scale—before constraints show up.

Businesses typically track a core set of cash flow metrics, including cash reserves, accounts receivable days, accounts payable timing and forecast accuracy. These KPIs provide insight into both current liquidity and future cash needs.

We use profit-focused accounting when helping our clients plan for growth. This approach breaks revenue into financial and non-financial drivers: elements of the business that are controllable and set through SMART goals (specific, measurable, achievable, relevant, and timely). These drivers then help our clients decide which measurable key metrics they need to determine if they are on the right track.

Key performance indicators act as levers business owners can “pull” to change course when their business plans seem to be derailing (such as the onset of a recession, client loss, etc.)

The KPI categories we recommend professional services firms track include:

- Cash

This blog post is part of a series that covers the profit-focused accounting metrics listed above. For this specific blog post, we are going to go over cash KPIs. Before we get into the details, we’d like to call out that graphics and tables included in this post are for example only. These should not be taken as industry averages.

Cash Flow KPIs and Metrics

Cash is king. It truly is the lifeblood of a business. Without cash, a business wouldn’t be in existence. In a recent pulse of business leaders who completed our Financial Maturity Assessment, many respondents reported having only enough cash to pay the bills each month — leaving little room for growth, investment or unexpected volatility. This is often the point where businesses realize they need more than basic accounting—they need forward-looking financial strategy. This is typically where companies begin working with a virtual CFO to translate cash flow data into planning, forecasting and decision-making.

That’s why cash is a KPI category chock-full of some of the most important financial data every business owner needs to be tracking. Let’s cover cash hygiene practices and KPIs that act as levers for your business.

Optimize Payment Terms

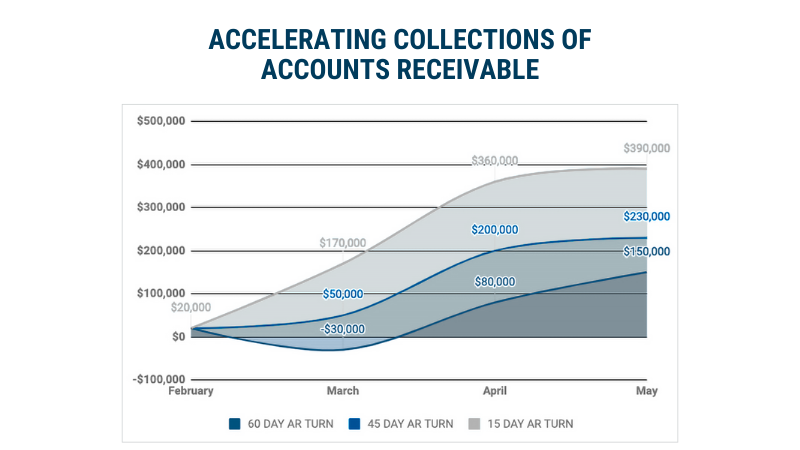

If you’re finding that you don’t have enough cash for day-to-day operations, start by adjusting your payment terms. Without changing pricing or selling additional services, you can regulate business cash flow by collecting payments at a quicker pace and improving your cash conversion cycle. We’d suggest decreasing your AR (accounts receivable) days from 60 down to 15 or 30 days. By doing so, cash inflows become more consistent, and you will no longer need to dip into your line of credit when cash is short. The below graphic gives an example of a company that ended up not needing to dip into their line of credit in March by reducing AR days to 15 days.

The impact of improving collections can be significant.

This is exactly why small shifts in timing—not just revenue—can change your cash position dramatically.

People are more likely to pay when they know payment due dates are tracked and missed payments are followed up accordingly. Businesses are also likely to pay on time when they have built a strong relationship with specific contacts at your company.

AR Policies

It is also worth developing an AR policy and notifying clients of what this policy entails from the beginning. For example, you could tell clients invoices must be paid within 15 days of the issue date or their services will be paused. Setting the policy is one thing but enforcing that policy is even more important. We recommend not compromising on these terms.

This might sound intimidating to have such strict payment terms, but these levers are designed to generate steady cash flow for your business.

Accounts Payable Processes

Cash flow hygiene isn’t only about managing inflows — it’s equally about managing cash outflows, too. To maintain a healthy and predictable cash cycle, take time to review and refine your supplier payment terms.

Where it makes sense, negotiate extended terms or adjust payment schedules so they better align with when you receive client payments. This approach helps reduce avoidable strain on your cash position and improves financial stability. The objective isn’t to pressure vendors, but to ensure your business maintains balance, control, and consistent liquidity.

Cash Reserve Levels: Are They Sufficient?

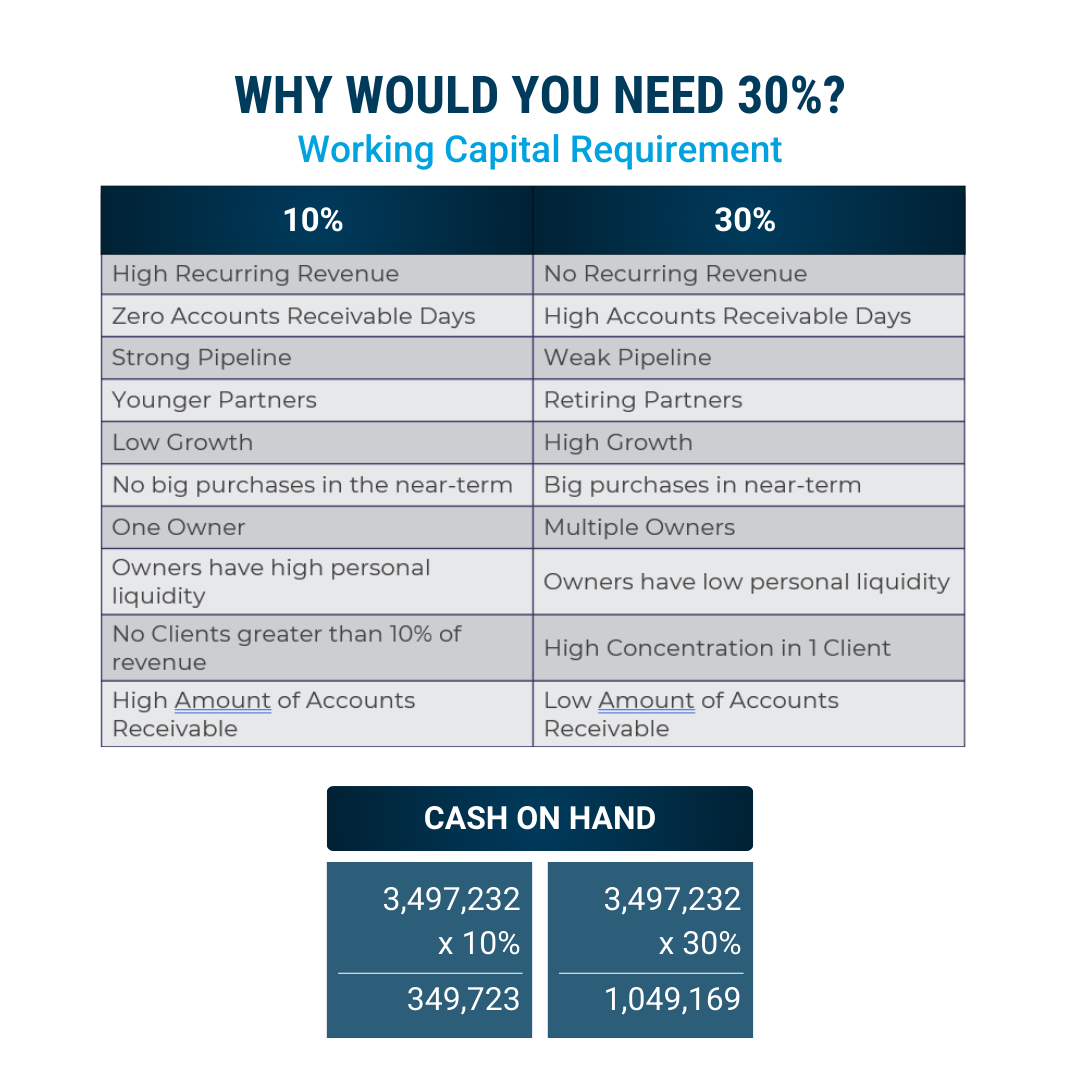

Every service-based business should keep around 10 to 30% of their yearly earnings stashed away in a cash reserve. This range is just a ballpark figure; there’s actually a formula to figure out the exact cash reserve you need (see below).

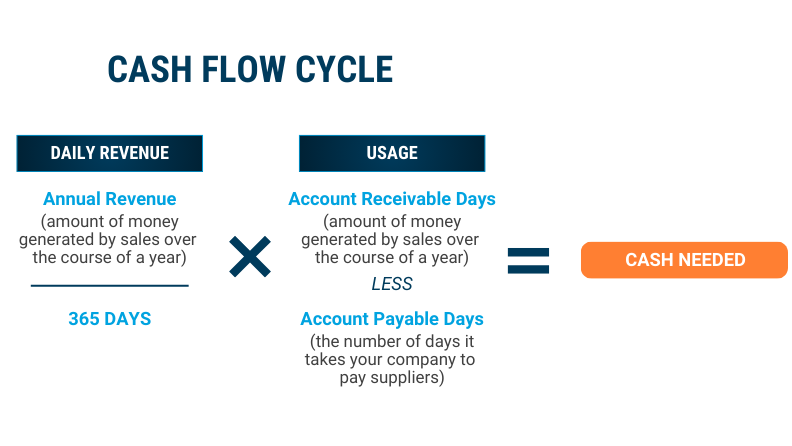

A simplified way to understand cash flow needs is through the cash flow cycle:

Even small changes in billing or payment timing can significantly impact how much cash your business needs to operate.

The framework above shows how revenue and timing—not just profit—drive cash requirements. If you want to translate this into a specific reserve target (and understand what pushes you toward 10% vs 30%), see How Much Cash Should a Business Have?

The amount of cash you choose to keep in reserve depends on your risk tolerance. For instance, keeping 10% equals roughly two months’ worth of expenses, while 30% covers about six months. Below is an example of a company earning $3,497,232 in revenue and the corresponding cash they should aim to have, based on their risk tolerance.

If your cash reserves aren’t sufficient, that’s a data point to pay attention to. Cash reserves provide a “plan B” for your business. When crisis hits, whether a major client leaves, a recession arrives, or a technology upgrade has to be taken care of NOW, you will have cushion to address these bumps before they become a mountain. On the other hand, if an unforgettable opportunity presents itself (such as the perfect candidate for a position you haven’t opened yet or a synergetic business acquisition comes your way), you will have cash on hand to take full advantage.

If your business doesn’t have a reserve built yet, now is the time to make a plan to build up the necessary funds.

Different business characteristics directly influence how much cash reserve is required.

These characteristics ultimately influence how far apart your cash inflows and outflows are—which is what drives your true cash requirement, not just revenue level. Businesses with more variability, growth or client concentration typically require higher cash reserves to maintain stability.

Forecast Accuracy: Is Your Forecast Measuring Up Against Actual Cash Flow?

When actual cash flow varies widely from your forecast, it usually signals a gap between your financial assumptions and how the business truly operates. The most common cause is timing—cash rarely moves in smooth, predictable patterns, even when revenue and profit look steady. Customer payment delays, inventory purchases, lump-sum expenses, debt payments, or seasonal swings all create volatility. In many cases, the issue isn’t poor performance—it’s a forecast that hasn’t been updated consistently or isn’t set up in a way that genuinely accounts for real-world variability.

Large variances between your cash flow forecast and actual cash flow become a red flag when there are unexplained causes or your forecast is consistently wrong. (If your forecast is consistently off, the fix is usually better inputs and a simpler update cadence—start here: Forecasting Your Business Cash Flow.) In the latter case, you need to redesign your forecast to reflect the true nature of your business and fluctuation factors that are consistent. Ultimately, meaningful cash flow forecasting isn’t about perfect prediction—it’s about continuously refining assumptions to better reflect how cash actually moves through your business. This is another point where businesses often benefit from working with a virtual CFO who can build and maintain accurate forecasting models.

Do We Have Many Unnecessary or Unused Expenses?

Have you heard any of those ads that talk about unused streaming or gaming subscriptions and how they can significantly impact your personal bank accounts? Well, just like personal bank accounts, business bank accounts are often chock full of charges for unused business products or software. It’s important that someone is monitoring these expenses to determine if they are necessary.

Cutting these expenses for more useful alternatives or removing them altogether will have a positive impact on your cash flow, freeing up funds for other initiatives.

Three Separate Bank Accounts – Three Purposes – Three Maintenance Levels

Businesses should have three separate bank accounts: an operating account, a cash reserve account, and a tax reserve account. If you can get your line of credit on a two-year cycle, that will be helpful in case of emergency or an opportunity that comes out of left field. Our quick math suggestion is to have the same amount in your line of credit as your cash reserve (if your bank will approve it).

You only want about two payrolls of cash in your operating account for working capital. The rest should be placed into your cash reserve. Putting that money in a high interest savings account, money market, or CD will keep your money safe while allowing you to generate a bit more cash off what is in the bank.

You should save 40% of your net income (your bottom line) for taxes. Put this money aside every quarter so it’s out of sight and out of mind. Don’t worry about a high tax bill—think of it as a sign that your business is doing well and making good profits.

If your line of credit, cash reserve, tax reserve, or operating cash flow account aren’t at their appropriate levels, this is a sign that you need to make adjustments to reach these goalposts for the financial health of your business.

If you need help turning these metrics into a cash flow strategy that supports growth, working with a virtual CFO can help you move from reactive decisions to proactive planning. For a deeper look at how forecasting supports long-term business performance, download our free guide, The Role of Dynamic Forecasting in Ensuring Business Growth.