Agency Cash Reserve Key Takeaways

- Most agencies should maintain 10–30% of annual revenue as a cash reserve

- Your target depends on risk, growth plans, and cash flow predictability

- This reserve supports working capital, growth opportunities, and emergency funds for unexpected costs

- Monitoring key metrics and updating forecasts regularly is essential to maintaining financial health

- Strong financial planning ensures your agency cash reserve supports—not limits—your long-term goals

A cash reserve is a percentage of revenue you put aside to overcome roadblocks or to take advantage of unexpected opportunities that come along. It functions as an emergency fund for your business and supports your day-to-day working capital needs when business finances are turbulent. For example, you might need to tap your marketing agency cash reserve for unplanned growth opportunities. Or you might need to tap your reserve if you incur unexpected costs and you need cash to pay your employees.

This question—“Do I have enough cash?”—is one of the most common (and stressful) questions agency owners face. Even after a strong year, uncertainty around hiring, investments, or future revenue can make it difficult to feel confident in your cash position. That’s exactly why having a clear reserve target matters: it provides both protection and decision-making clarity and is a key part of overall financial planning.

Your cash reserve should fall somewhere between 10–30% of your annual revenue. We will show you how to calculate exactly what amount of cash you need to keep aside in your cash reserve.

As a general benchmark:

- 10%: Stable businesses with predictable revenue and short cash cycles

- 20%: Moderate growth with some variability

- 30%: High growth, inconsistent revenue, or higher risk

It’s also important to note that what you have in your cash reserve depends on how much risk you are willing to take, as well as your growth plans, revenue predictability, and access to capital. Your reserve needs will vary based on these factors. 10% equals roughly two months of operating expenses, while 30% covers about six months of operating expenses.

You can think of your cash reserve like fuel for a road trip: it allows you to keep moving toward your goals without running into trouble if conditions change. The more uncertainty in your journey, the more fuel you’ll want to carry to protect your financial health.

How Do I Calculate My Ideal Cash Reserve?

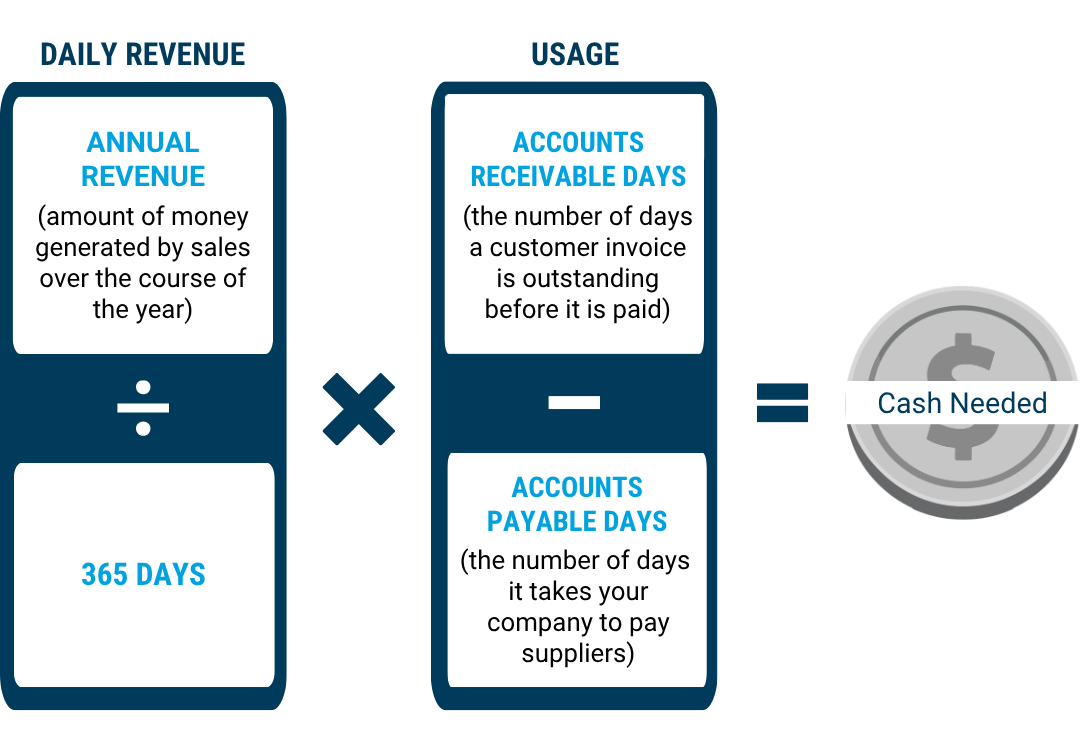

To determine the cash reserve your agency should ideally have, follow our formula below.

Basically, you will calculate two numbers and multiply them. Start by dividing annual revenue by 365 – this gives you your average daily revenue. Then, subtract accounts payable days from accounts receivable days: this number represents your cash usage, the amount of time you need to have your bills (AP) covered before your cash comes back in the door (AR). Take these two numbers, and multiply. Now you know how much cash should be in your reserve.

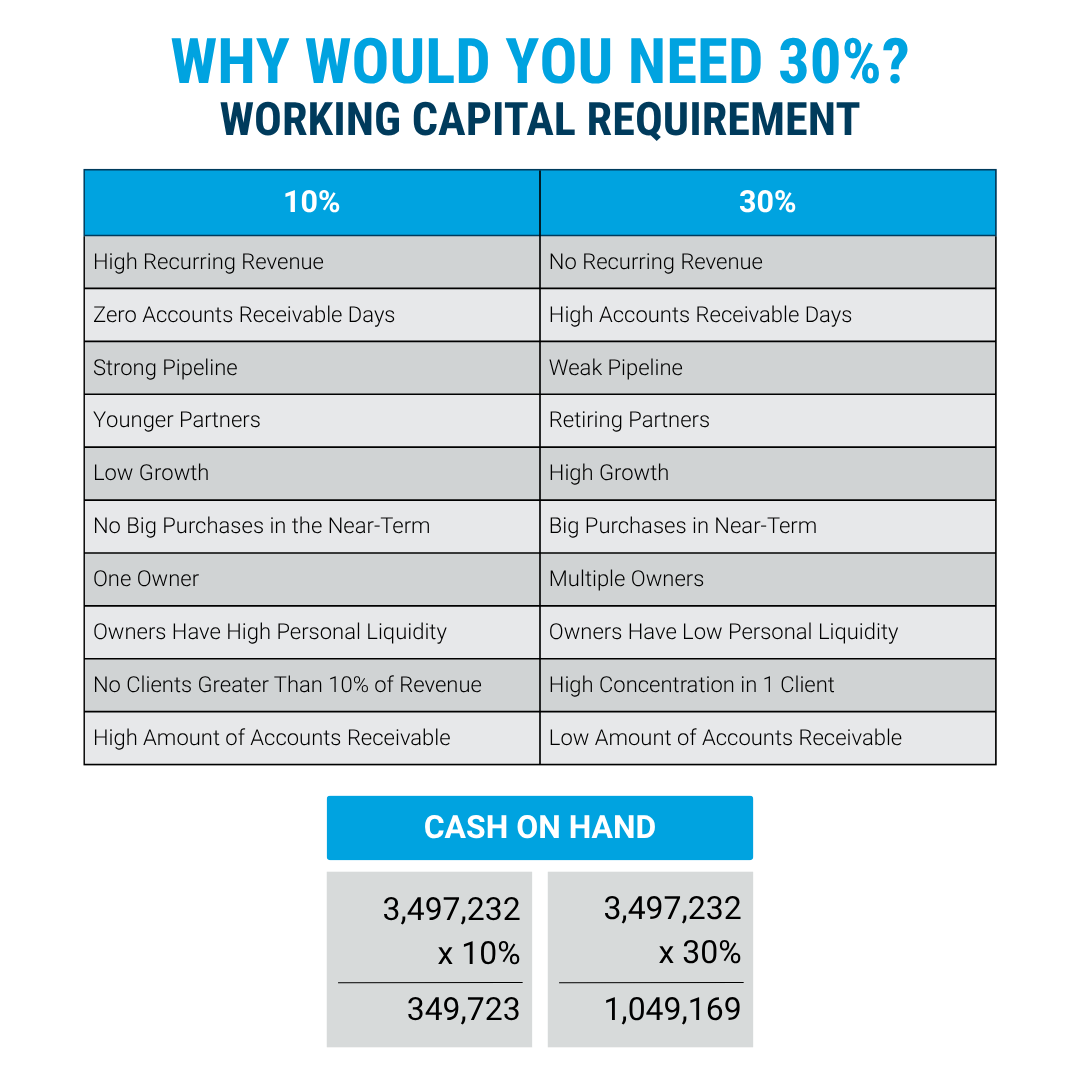

Now remember, we said that you may want more money in your account if you are a little bit more on the conservative side when it comes to risk – or if your agency fits any of the criteria outlined below.

It’s also worth noting that this calculation isn’t one-and-done. As your revenue grows, your client mix changes, or your strategy shifts (for example, toward scaling or preparing for an exit), your agency cash reserve target should evolve as well. Strong cash flow management is one of the most important financial metrics to monitor, and ongoing adjustments are part of maintaining long-term financial health.

What Impacts Where You Fall in the Range?

However, there are factors that might make you want to move your number up or down, based on the likelihood of needing cash in the near future.

All the factors on the 10% side of the chart point to an agency with steady cash flow, a low chance of needing large sums of cash on short notice and a good backup plan in case they do (i.e. owner liquid assets). These agencies have:

- A diverse client base (no single client dominating revenue)

- Strong billing processes and short cash cycles

- A strong pipeline and high close rate

- Low growth or no major upcoming investments

These agencies aren’t as dependent on a single win to stay afloat and can convert effort into cash relatively quickly, which reduces the need to hold excess cash that could otherwise be reinvested into the business.

The factors on the 30% side of the chart point to an agency that has more ups and downs, which makes it more susceptible to individual clients and market whims. These agencies often have:

- Longer cash cycles or inconsistent billing practices

- Higher client concentration or turnover

- Aggressive growth plans or upcoming large investments

- Multiple owners or lower personal liquidity

They may have a thick book of business but a high number of Accounts Receivable Days. Agencies that are planning to scale will also be on the higher end of the spectrum, since they should expect large outflows (and unexpected costs) before seeing increases in revenue.

Simply put: the more variability, risk, or growth in your business, the more cash you need to protect profitability and maintain momentum.

Cash also plays a critical role in resilience. During periods of economic disruption, businesses with stronger cash reserves are better positioned to absorb shocks without making reactive decisions that could hurt long-term performance.

Don’t Forget About Access to Capital

Regardless of where you fall on the 10–30% spectrum, you’ll want to have a line of credit in an equal amount – and you’ll want to secure it well before you need it.

The line of credit can save the day if your short-term cash flow suggests that your AP will be higher than your AR for a certain period. You’ll pay it off as soon as the cash comes in, but you’ll keep your vendors and employees happy in the meantime.

Think of this as an additional safety net. Your cash reserve is your first line of defense; your line of credit is your backup plan.

Keep Your Agency Cash Reserve in a Separate Bank Account

Once you have a cash reserve number, we recommend building towards it and, as you do so, using a separate account from your tax account and operating account. This makes it easier to view it as its own, separate entity – which makes cash flow management easier.

As a best practice, many businesses maintain:

- An operating account (with ~2 payrolls worth of cash)

- A reserve account (for your cash reserve)

- A tax account (for estimated tax payments)

Since the dollar amount will be relatively high, put your cash reserve in an account that can make you a bit more interest. This might be a high-interest savings account or money market account for example—something low-risk but accessible while still earning a return.

Supporting Your Cash Position Over Time

Once you’ve established your reserve target, the next step is maintaining it. A strong business model doesn’t automatically guarantee strong cash flow—process matters.

A few key habits that help marketing agencies protect and build their reserves:

- Improve billing hygiene: Invoice promptly, shorten payment terms, and consider retainers or deposits

- Use forecasting regularly: A dynamic, updated cash flow forecast allows you to make informed decisions as conditions change

- Plan for taxes consistently: Setting aside funds throughout the year avoids surprises and protects your reserve

- Maintain strong financial processes: Clear roles and accountability reduce errors and improve visibility

For a deeper breakdown of how to calculate and adjust cash targets across any business, see How Much Cash Should a Business Have?

A forecast, in particular, is what turns a cash reserve from a static number into a strategic tool. It gives you confidence not just in how much cash you have—but in what you can safely do with it, including reinvesting excess cash into the business when appropriate.

If you’re unsure whether your cash position supports your growth goals, it may help to step back and look at how cash, forecasting, and decision-making connect in your agency. Our maturity assessment can help you identify where your financial foundation is strong—and where it needs to evolve.